The latest economic outlook report highlights a troubling trend within the West African Economic and Monetary Union (WAEMU): while regional banking has reached symbolic milestones, it is increasingly undermined by a growing wave of financial instability. At the epicenter of this crisis lies Niger, whose staggering non-performing loan (NPL) rate has singled it out as a critical weak link in an otherwise fragile monetary bloc.

Niger’s Banking Sector: A Distress Signal for the Region

As WAEMU strives to reinforce financial stability, Niger remains an outlier with the most alarming asset degradation metrics in the union. Despite marginal improvements, the country continues to represent the most vulnerable component of the regional banking system.

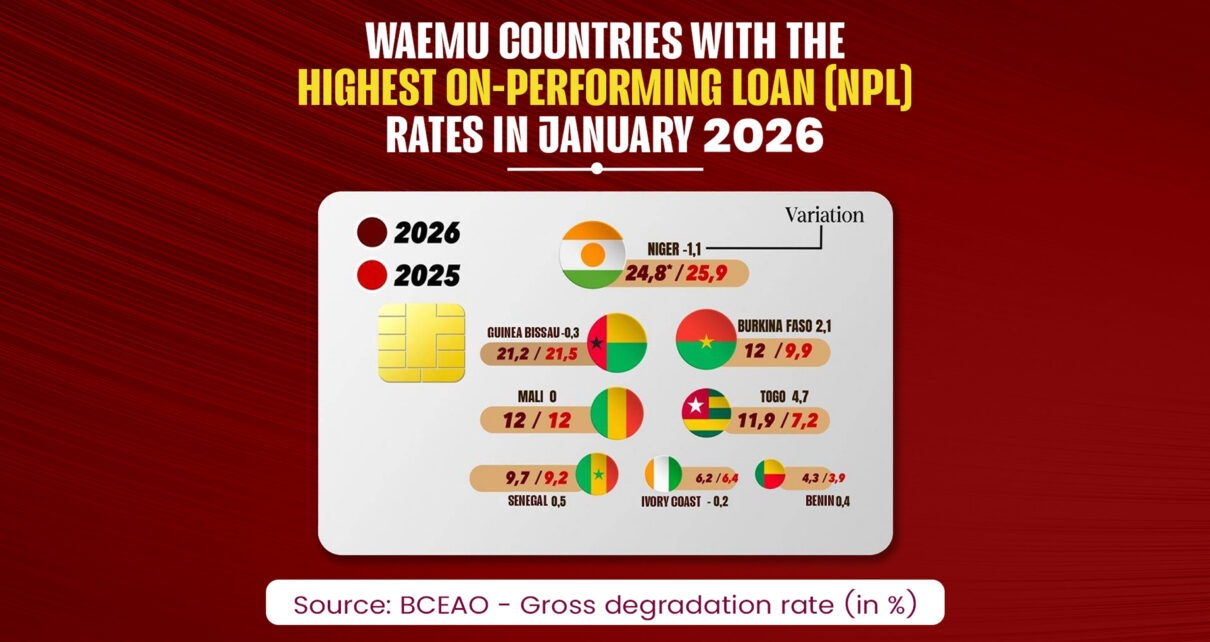

With an NPL ratio of 24.8% as of January 2026, Niger holds the unenviable distinction of leading the regional ranking. This means nearly one in four loans disbursed in the country is now in default—a figure that, while slightly down from 25.9% in 2025, still far exceeds the regional average. The persistent gap underscores systemic vulnerabilities exacerbated by security challenges and political instability.

A Divided Union: Coastal Stability vs. Sahelian Instability

The January 2026 data underscores a stark disparity between the economic resilience of coastal nations and the growing financial distress in the Sahelian bloc, where Niger serves as the crisis’s focal point.

The Sahel’s Growing Credit Crunch

Beyond Niger, other Sahelian countries are also grappling with soaring NPL rates:

- Mali and Burkina Faso: Both report a 12% NPL ratio, with Burkina Faso experiencing a sharp year-on-year increase of 2.1 percentage points.

- Guinea-Bissau: Remains mired in critical territory at 21.2%.

A Coastal Exception: Stability with Caution

In contrast, coastal members of the union have demonstrated greater resilience, though not without challenges:

- Benin: Leads the region with the lowest NPL rate at 4.3%, setting a benchmark for fiscal prudence.

- Senegal and Côte d’Ivoire: Maintain relative stability at 9.7% and 6.2%, respectively.

- Togo’s Outlier Status: Defies regional trends with an NPL surge from 7.2% to 11.9% (+4.7 points), raising concerns about its financial trajectory.

Systemic Pressures: Credit Expansion Meets Rising Defaults

The union’s total loan portfolio has crossed a historic threshold of 40.031 trillion FCFA, reflecting a 4.7% annual growth. However, this expansion is overshadowed by a mounting tide of bad debt, which has now reached 3.631 trillion FCFA—a record high.

The financial strain is further evidenced by a provisioning coverage ratio that has dipped to 59%, signaling that banks are struggling to keep pace with the accelerating rate of defaults. This erosion of safeguards raises red flags about liquidity risks across the monetary zone.

Banks Tighten the Reins: Credit Caution Takes Priority

In response to the deteriorating risk profile—particularly in high-default regions like Niger—financial institutions are adopting more conservative lending practices:

- Stricter lending criteria: Increased down payment requirements and enhanced collateral demands.

- Selective credit allocation: Banks are prioritizing balance sheet security over the expansion of credit to local SMEs/PMEs, potentially stifling economic dynamism.

As of early 2026, the WAEMU banking system stands at a crossroads. While the union’s overall financial health remains intact, the escalating crisis in Niger and its spillover effects across the Sahel demand heightened vigilance to avert a potential regional liquidity crunch.